Introduction As mortgage loan originators, we’re the compass guiding potential homebuyers through the ever-changing terrain of real estate financing. In today’s dynamic market, let’s address misconceptions head-on and empower buyers with accurate information. Buckle up; we’re diving deeper! 1. The Ultra-Low-Rate Anomaly: Lessons from Recent Turbulence Scenario: The Pandemic Rate Drop Remember those jaw-dropping mortgage rates during the COVID-19 pandemic? Buyers were practically doing cartwheels. But here’s the truth: that was an exceptional period, not the norm. Let’s educate our clients:

Samantha Shelton, founder of Michigan-based Align Lending, weathered the storm of 2022 and 2023. She explains, "As tough as the market has been, there is tremendous opportunity out there right now." Originators who preserved are witnessing signs of a turning market. Samantha's advice: "Double down on education and leverage tools for success." 2. What a Healthy Market Looks Like: Beyond Interest Rates Scenario: Balanced Supply and Demand A healthy market isn't solely about rates. Let's debunk the myth that low rates define market health:

In January, US new home sales increased by 1.5%, buoyed by lower mortgage rates. The annualized pace reached 661,000, slightly below expectations. This demonstrates a more balanced market where buyers can make confident decisions. 3. Confidence-Building Insights: Empowering Buyers Scenario: Educating Buyers for Long-Term Vision Our role extends beyond transactions. Let's empower buyers:

Buyers who understand market cycles and focus on long-term goals thrive. As originators, we provide context, transparency, and confidence-building insights. Our clients appreciate honesty and informed decision-making. Conclusion: Navigating with Confidence

In 2024, we're poised for wins. The market is turning, and educated buyers are ready. Remember, a healthy market isn't just about rates - it's about stability, knowledge, and achieving homeownership dreams. Let's guide our clients with clarity and confidence.

0 Comments

The National Association of Realtors (NAR) recently reached a landmark $418 million settlement arising from an inflated commission fees lawsuit. This agreement is expected to profoundly influence the real estate market. Pending approval by a federal court, industry experts anticipate substantial changes from this settlement. Potential Changes Resulting from the Settlement Commission Structure Revolution: The settlement aims to eliminate traditional real estate brokers' commissions, which have historically been as high as 6% of the purchase price. Instead, home buyers and sellers will now have the ability to negotiate fees directly with their agents upfront. Potential Fee Reduction: Real estate fees could drop by as much as 30%. This reduction in fees may lead to significant cost savings for both buyers and sellers. Impact on Real Estate Agents: The ranks of real estate agents are expected to thin out, further driving down commission prices. With the removal of standard commissions, agents may need to adapt to new fee structures and negotiate their compensation directly with clients. Consumer Choice and Protection: The settlement aims to preserve consumer choice while protecting the interests of NAR members. By allowing more flexibility in fee negotiations, consumers can make informed decisions about their real estate transactions. Changes in MLS Practices: Currently, home sellers are locked into paying brokerage fees for listing their properties on multiple listing services (MLS). The settlement will strip brokerage commissions from MLS sites, opening opportunities for negotiation with sellers. Buyers may benefit from greater access to property listings without being tied to standard brokerage commissions. Reduced Costs: With the elimination of traditional real estate commissions, buyers can potentially save money. The reduction in fees may allow them to allocate more funds toward their home purchase or other expenses. Negotiation Power: Buyers will now have the ability to negotiate fees directly with their agents upfront. This empowers them to seek more favorable terms and ensures transparency in the transaction. Increased Choice: The settlement aims to preserve consumer choice. Buyers can explore a wider range of agents and fee structures, selecting the one that best aligns with their needs and preferences. How Do These Changes Differ from Current Practice? Shift in Responsibility: Currently, sellers typically cover the commission for both their own agent and the buyer's agent. However, the settlement aims to change this. Sellers may no longer be obligated to pay for the buyer's agent commission, potentially shifting that responsibility to buyers. Negotiation Upfront: When working with a real estate agent, negotiate the commission rate upfront. Even a small reduction in the agent's fee can lead to significant savings. For instance, lowering a 6% commission to 5.5% on a $500,000 home sale would save you $2,500. Market Adjustment: It remains to be seen how these changes will impact home sales. Some experts predict that prices may adjust - either going up for buyers or correcting themselves over time. An adjustment period is likely as buyers, sellers, and agents adapt to the new landscape. Impact on the Mortgage Industry Traditional Commission Structure: Historically, real estate commissions were built into the sales price. Sellers paid both their own agent's commission and the buyer's agent's commission. These commissions were typically around 6% of the home's sale price. The buyer's agent's commission was indirectly covered by the seller, affecting the overall transaction cost. Settlement's Impact on Buyer's Agent Commissions: Under the new settlement, buyers, not sellers, will decide how much buyer's agents are paid. This means that buyers can directly negotiate fees with their agents. While this change allows for more transparency, it also alters the traditional financing structure. Potential Financing Implications: When buyers pay their agents directly, the sales price may not include the buyer's agent's commission. As a result, the mortgage amount requested by the buyer may be lower. Lenders typically base mortgage approvals on the sales price, so if the commission is excluded, the financing amount could differ. Navigating the Transition: It remains to be seen how lenders will adapt to this shift. Buyers should communicate openly with their lenders about the direct payment to their agents. Lenders may need to adjust their calculations to ensure that buyers receive the appropriate financing. Summary

In summary, this settlement has the potential to reshape how millions of sellers and buyers transact in the real estate market, with implications for agent commissions and industry practice. The settlement could also introduce flexibility and cost savings. Buyers and lenders will need to navigate the transaction to ensure that mortgage financing aligns with the new commission structure.  The mortgage industry is a complex and ever-evolving landscape. As a mortgage professional, staying ahead means not just keeping up with the changes but also proactively expanding your business opportunities. One such strategic move that can significantly enhance your market presence is obtaining mortgage originator licenses in multiple states. This endeavor, while demanding, can open doors to a plethora of opportunities and advantages. Understanding the Licensing Landscape Before embarking on this journey, it's crucial to understand the licensing landscape. The Nationwide Mortgage Licensing System and Registry (NMLS) is the gateway to your multi-state licensing process. It's a one-stop-shop for managing your mortgage licensing requirements across the United States. The National Exam with Uniform State Content (also known as UST) The first step is to pass the National Exam with UST. This exam tests your knowledge of federal laws, general mortgage principles, mortgage loan origination activities, and ethics. The UST component ensures your have a baseline understanding of state-specific regulations. Pre-Licensing Education Required The NMLS mandates a 20-hour pre-licensing education, which includes:

State-Specific Requirements Each state has its own set of additional requirements. These can include extra educational hours focused on state laws and practices, state-specific exams, or even unique application processes. It's imperative to research each state's requirements thoroughly to ensure compliance. The Financial Commitment The financial commitment to obtaining multi-state licenses is not insignificant. Here's a more detailed breakdown of the potential costs involved: NMLS Processing Fees

The Strategic Advantages of Multi-State Licensing With the costs laid out, let's explore the strategic advantages of holding licenses across multiple states: Business Expansion By obtaining licenses in various states, you're not just expanding geographically; you're also broadening your potential client base. This expansion allows you to tap into new markets and cater to a diverse clientele. Market Diversification Diversification is a fundamental principle in business. By operating in multiple states, you mitigate the risks associated with economic downturns or regulatory changes in any single market. Enhanced Credibility and Expertise Holding multiple state licenses showcases your dedication to your profession and your expertise in the field. It signals to clients and peers alike that you're a knowledgeable and reliable mortgage professional. Servicing Relocating Clients In today's mobile society, clients often move across state lines. With licenses in multiple states, you can continue to service your clients, providing continuity and building long-term relationships. Competitive Edge In a competitive industry, every advantage counts. Multi-state licensing allows you to compete with larger banks and financial institutions, giving your an edge in both service and reach. Conclusion The path to multi-state mortgage licensing is a journey of commitment, investment, and strategic planning. The benefits, however, are clear and compelling. From business growth to market resilience, the advantages of holding multiple state licenses can significantly impact your success as a mortgage professional.

Remember, this blog post is a high-level overview and should not be taken as financial advice. Always consult with the NMLS or a professional in the field for the most accurate and up-to-date information. Happy Licensing! If you have any questions pertaining to multi-state licensing or licensing in general, please feel free to reach out to one of our concierges.  When evaluating the evolving job landscape of 2024, choosing a career path that offers security, growth, flexibility, and financial stability is more crucial than ever. Among the myriad of options, becoming a mortgage loan officer offers a compelling choice, especially when compared to other professions such as those int he tech industry, healthcare, education, and sales and marketing. Let's delve deeper into why becoming a mortgage loan officer could be the smart move in today's economic landscape. Unveiling Financial Incentives Financially, a career as a mortgage loan officer is compelling. The combination of a base salary supplemented by performance-based commissions offers lucrative earning potential that can rival or even surpass many professions. For instance, while tech industry roles like software engineers boast higher average starting salaries, the earnings ceiling in mortgage lending can be limitless, hinging on one's ability to cultivate relationships and close loans. In contrast, educators, and healthcare workers, despite their invaluable societal contributions, often face capped earnings and rigid salary scales that limit growth. While the median annual wage for loan officers was around $63,270, those in the top 10 percent earned more than $132,080, according to the latest data from the U.S. Bureau of Labor Statistics (BLS). The Educational Pathway The educational pathway to becoming a mortgage loan officer is markedly streamlined compared to other professions. A high school diploma might suffice, but a bachelor's degree in finance or a related field can give candidates an edge, whereas careers in healthcare and tech demand extensive, specialized education. The requisite Mortgage Loan Originator (MLO) license, obtained through completing pre-licensure courses, passing an exam, and fulfilling background checks, is more straightforward than the extensive schooling and residency required for doctors or the rigorous technical training for software engineers, and without student debt than can burden other career paths. Future Outlook: A Landscape of Opportunity Looking forward the mortgage lending industry is ripe with opportunity. The fundamental desire for homeownership remains a constant, driving demand for mortgage loans regardless of economic fluctuations. This enduring need ensures a steady flow of clients and a resilience that careers heavily influenced by technological disruption or policy changes - such as those in the tech and healthcare sectors - might not enjoy. Moreover, the evolving landscape of digital lending and financial technology presents a frontier for innovation within the field, offering mortgage loan officers the chance to leverage new tools to enhance and client service.  Flexibility and Entrepreneurial Spirit A distinct advantage of the mortgage loan officer career is its inherent flexibility. Unlike many professions tethered to the traditional office environment or the rigid schedules of healthcare and education sectors, mortgage loan officers often have the autonomy to set their own schedules, work remotely, and thus achieve a desirable work-life balance. This career path also caters tot he entrepreneurial spirit, allowing individuals to build and grow their own client base, essentially running their own business with the support of their employing financial institution. Leveraging Digital Advancements In an era defined by digital transformation, the mortgage industry is no exception. The rise of online applications, automated underwriting, and digital documentation has streamlined the mortgage process, enabling loan officers to focus more on client relationships and less on paperwork. Those who embrace these tools can differentiate themselves int he market, offering faster, more efficient service and a better overall customer experience. A Comparative Analysis When measured against the backdrop of other professions, the role of a mortgage loan officer is distinguished not just by the potential for high earnings and growth, but also by the unique benefits it offers in terms of flexibility, work-life balance, and the satisfaction of helping individuals and families achieve their homeownership dreams. While careers in tech, healthcare, education, and marketing each have their own merits and attractions, the mortgage lending field stands out for those who value independence, financial opportunity, and the ability to directly impact people's lives in a positive way. In Conclusion As we look at the job market of 2024 and beyond, becoming a mortgage loan officer presents a compelling career choice that marries financial reward with personal satisfaction. With its manageable entry requirements, robust earning potential, and forward-thinking industry outlook, this career path offers a promising horizon for those ready to embrace its opportunities. Whether you're just starting out or looking to pivot into a career that offers more autonomy and the chance to thrive, the mortgage lending field stands as a bright spot of professional options.

Market Dynamics and Analysis The 2024 U.S. housing and rental markets present a complex and ever-evolving landscape. For mortgage professionals, understanding and adapting to these changes is key to success. This guide delves into strategies and insights for mortgage professionals working in these dynamic markets. Housing Market Overview Regional Market Disparities: An in-depth understanding of disparate regional housing trends is imperative. For example, knowing the economic drivers behind the growing markets in the South versus the stability of the Midwest is critical for mortgage structuring. Housing Segmentation: Understanding segmentation of the housing market into luxury, mid-tier, and affordable segments enables tailored financial solutions. Each segment presents distinct economic behaviors and risk profiles requiring specialized market products. Rental Market and Investment Opportunities Rental Market Dynamics: With a surge in rental demand, opportunities in investment property financing are expanding. An understanding of these dynamics, including yield rates and occupancy risks, is essential. Rent-to-Own Financial Structuring: Mastery of rent-to-own agreements offers a strategic avenue for facilitating homeownership, particularly in transitional economic periods. Advanced Operational Strategies Diversified Financing Solutions Comprehensive Loan Portfolio Management: Developing a diverse portfolio of loan products, from FHA to adjustable-rate mortgages, allows for strategic alignment with varied client financial requirements. Refinancing Strategies in Flux Markets: In an environment of fluctuating interest rates, proactive refinancing advisement can optimize clients' financial positions while fostering long-term client loyalty. Elevated Client Education and Advisory Buyer Education Programs: Implementing comprehensive educational programs on homeownership and mortgage intricacies, tailored to different buyer segments, enables informed decision-making, and builds long-term business relationships. Investment Property Advisory: Offering in-depth consultation on real estate investment, including informed market analysis and portfolio diversification strategies, caters to a growing segment of real estate investors. Technological Integration and Data Utilization Technology Advancements: Leveraging cutting-edge property technology platforms for loan processing and client interactions enhances operational efficiency and client engagement. Predictive Analytics and Personalization: Utilizing vast data for predictive analysis and personalized mortgage solutions aligns client financial profiles with market conditions. Sustainable and Green Financing Expertise Green Mortgage Specialization: Developing expertise in green mortgages, including understanding of environmental certifications and energy-efficient property standards, caters to a growing eco-conscious market segment. Collaboration with Sustainable Developers: Forming strategic partnerships with developers focused on sustainable projects aligns with market trends and broadens the client base.   Strategic Networking and Relationship Management Industry Collaboration and Synergies Real Estate Partnership Synergies: Establishing collaborative relationships with real estate professionals not only facilitates referrals but also enhances market knowledge and client service. Community and Industry Integration: Active participation in industry forums and local housing initiatives solidifies a reputation as a knowledgeable and committed mortgage professional. Advanced Client Relationship Management Relationship Lifecycle: Implementing a targeted approach to client management that affects the entire homeownership process, from initial purchase to subsequent investments or refinancing. Customized Client Experiences: Utilizing advanced CRM tools for delivering tailored client interactions based on detailed client profiles and historical data. Policy Engagement and Advocacy In-Depth Policy and Regulatory Knowledge Regulatory Insight and Compliance: Maintaining a deep understanding of evolving housing regulations and compliance requirements ensures the client is always properly advised and promotes operational integrity. Proactive Industry Advocacy: Engaging in policy discussions and contributing to industry dialogue to shape favorable legislative outcomes for homeownership and mortgage accessibility establishes the mortgage professional as an elite industry leader.  Business Growth and Market Positioning Strategic Market Expansion Identifying Emerging Market Opportunities: Analyzing demographic shifts, economic indicators, and housing developments to identify and capitalize on emerging market opportunities. Service Diversification: Exploring adjacent markets and additional services, such as commercial lending or insurance offerings, diversifies the mortgage professional's business while creating additional revenue streams. Sophisticated Marketing and Brand Development Robust Digital Marketing Strategy: Developing a comprehensive digital marketing strategy, including SEO-optimized content and targeted social media campaigns, to enhance a mortgage professional's market reach and brand visibility. Reputation Management and Community Presence: Cultivating a strong professional reputation through exemplary service . thoughtful leadership, and community involvement establishes trust and positions the mortgage professional as an industry authority. For mortgage professionals navigating the complex and evolving U.S. housing market, success hinges on a multifaceted strategy encompassing market knowledge, diversified product offerings, utilization of advanced technology, and robust client and community engagement. Embracing these principals will enable professionals to not only navigate but also excel in these markets, providing exceptional service and strategic guidance to clients in their real estate needs.

Everyone is talking about AI (Artificial Intelligence) and how today's companies will need to make AI an integral part of their operations or struggle to compete. What does that mean for the mortgage industry? We've all been using Desktop Underwriter (DU) and Loan Prospector (LP) for years, but is it likely AI will need to be integrated into all aspects of the business? Many predict that this technology is not just an advantage but a necessity, AI stands out as a game-changer for the mortgage industry. As a mortgage loan originator, integrating AI into your business can revolutionize not only how you work but also the service you provide to your clients. Let's delve into how AI can enhance different facets of your mortgage business. Automated Pre-Approval Process

Round-the-Clock Customer Service

Advanced Risk Assessment

Targeted Marketing and Sales

Streamlining Document Processing

Predictive Analytics for Market Trends

Continuous Learning for Service Improvement

Cost Efficiency

Compliance and Regulation Adherence

Conclusion Incorporating AI into your mortgage business is not just about keeping up with technology - it's about setting a new standard in service and efficiency. By adopting AI, you can offer faster, more accurate, and personalized services, transforming the way mortgages are handled and setting your business apart in this competitive industry. Stay ahead of the curve and embrace AI - your clients, and your bottom line, will thank you.

The mortgage industry has witnessed significant changes in homeowners insurance over the last two decades, particularly in the rising costs and the increasing percentage of the average mortgage payment devoted to homeowners insurance. This blog aims to delve into these changes, analyzing the reasons behind them. Evolution of Homeowners Insurance Costs Rising Insurance Premiums Over the past twenty years, homeowners insurance premiums have seen a steady increase. This rise can be attributed to several factors, including increased property values, the rising cost of construction materials, and labor. As homes become more expensive to build and repair, insurance companies have adjusted their premiums to reflect these higher costs. Increased Frequency of Natural Disasters There has been a noticeable uptick in the frequency and severity of natural disasters, such as hurricanes, floods, wildfires, and tornadoes. These events lead to massive insurance claims, forcing insurance companies to raise premiums to cover these losses. Climate change is often cited as a contributing factor to this trend, indicating that this may be a continuing challenge in the future. Changes in Building Codes and Regulations Building codes and regulations have become stricter over the past two decades, often requiring more expensive building materials or techniques. This increase in building standards, while beneficial for safety and efficiency, has also led to higher reconstruction costs, subsequently affecting insurance premiums. Impact on Mortgage Payments Increased Proportion of Insurance in Mortgage Payments Traditionally, homeowners insurance has been a smaller component of the overall mortgage payment. However, with the rising insurance costs, this proportion has significantly increased. For many homeowners, particularly in high-risk areas, insurance can now constitute a substantial part of their monthly mortgage expenses. Affordability Concerns The increased cost of homeowners insurance has added to the overall affordability challenges in the housing market. For prospective buyers, especially in regions prone to natural disasters, the combined cost of mortgage and insurance can be prohibitive, impacting the accessibility of homeownership. Analyzing the Reasons Behind These Changes Economic Factors Economic inflation over the past two decades has impacted virtually every industry, including housing and insurance. The general rise in the cost of goods and services naturally extends to the components that affect homeowners insurance. Insurance Risk Assessment Changes Insurers have become more sophisticated in their risk assessments, using advanced technology and data analytics. This improved precision often leads to higher premiums for areas deemed higher risk, reflecting a more accurate understanding of the potential cost of claims. Regulatory and Industry Changes The insurance industry has undergone numerous regulatory changes. These changes aim to ensure the solvency and reliability of insurance providers but can also lead to increased operational costs for these companies, which are often passed on to consumers. Consumer Expectations and Coverage Enhancements As consumer expectations for comprehensive coverage have increased, insurance products have evolved to offer more extensive protection. These enhancements, while beneficial, also contribute to higher premiums. Over the Last 20 Years, How Much has Insurance Cost Risen? To compare the homeowners insurance cost for a $400,000 home in 2003 and 2023, we need to consider several factors that influence the cost of insurance. Please note that the actual insurance cost can vary significantly depending on location, the specifics of the home, the level of coverage, and other risk factors. The following comparison uses generalized assumptions and averages for illustrative purposes. Homeowners Insurance Cost Comparison Insurance Cost for a $400,000 home in 2003, assuming standard coverage, average location, moderate risk factors. Estimated Annual Premium: Given historical data trends, the annual premium for a $400,000 home in 2003 could have been approximately $800 to $1,200. This is a rough estimate and would vary based on location and other factors. Insurance Cost for a $400,000 home in 2023 with similar coverage levels, adjusted for inflation and increased building costs. Estimated Annual Premium: The annual premium in 2023 for a similar $400,000 home could be significantly higher, possibly in the range of $1,800 to $2,500 or more. Important Considerations Inflation and Economy: The rate of inflation and economic changes over 20 years can significantly impact insurance costs. Risk Adjustments: Changes in environmental risk (like increased frequency of natural disasters) and other risk factors (like crime rates) can affect insurance premiums. Coverage Adjustments: Homeowners may opt for different levels of coverage, affecting costs. Location-Specific Factors: Insurance rates can vary greatly by state and even within different areas of a state. Conclusion

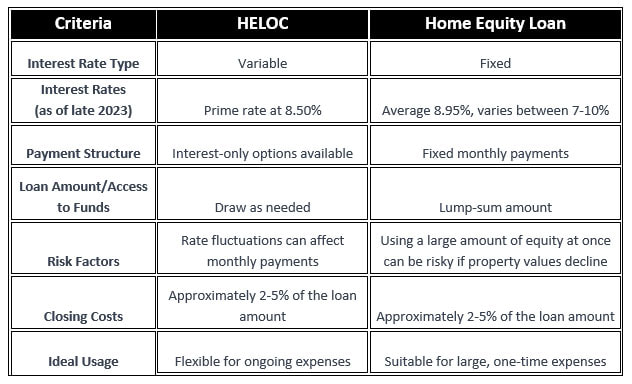

The past two decades have seen a significant shift in the landscape of homeowners insurance, impacting both the industry and homeowners. The increase in insurance costs, influenced by a multitude of factors ranging from environmental changes to economic inflation, has altered the composition of mortgage payments, emphasizing the need for industry adaptation and consumer awareness. As the industry continues to evolve, understanding these changes will be crucial for both mortgage professionals and homeowners alike.  As mortgage professionals, we often encounter homeowners seeking to tap into their home equity for various financial needs. Two popular options are a Home Equity Line of Credit (HELOC) and a Home Equity Loan (HELOAN). Both have their unique features, benefits, and considerations. Here's a detailed guide to help them make an informed decision. Current Interest Rates: A Snapshot As of late 2023, interest rates for these products are as follows: HELOC: The average rate for a 10-year HELOC hovered around 5.95% at the end of 2022, reaching a high of 6.62% and a low of 3.96% earlier in the year. Currently, the prime rate for HELOCs is at 8.50%. HELOAN: The average interest rate for a home equity loan is approximately 8.95%. Rates typically range between 7% and 10%, with average rates for fixed-rate home equity loans at 7.87% for 15 years and 7.93% for 10 years. Analyzing the Pros and Cons Home Equity Loans Advantages:

HELOC Advantages:

Understanding Costs Both options involve closing costs, generally ranging from 2% to 5% of the loan amount. While these costs are lower than those for a primary mortgage, they are a significant factor in one’s overall financial planning. Personalized Advice As mortgage experts our advice should be tailored to individual circumstances. Consider the following:

HELOC vs. Home Equity Loan Comparison Chart  Additional Notes:

Disclaimer: The information provided is based on rates available as of late 2023. Rates are subject to change. Consumers are advised to consult with a financial advisor for personalized advice. Final Thoughts The decision between a HELOC and a Home Equity Loan depends on the individual’s financial goals, risk tolerance, and the specific use of the funds. Remember, tapping into home equity is a significant financial decision. It's essential to consider the impact on one’s overall financial health and long-term goals. Consulting with a trained financial advisor can provide additional insights tailored to one’s unique situation. As always, mortgage professionals are here to help guide an individual through these decisions, ensuring you choose the best path for your financial future.

The rise of automated underwriting systems such as Desktop Underwriter or Loan Prospector have significantly transformed the mortgage industry. Despite the increased reliance on these systems, there remains a strong and growing need for skilled mortgage loan underwriters. This blog post explores the career benefits of becoming a mortgage loan underwriter in the current technological landscape. The Role of Technology

Career Benefits of Being a Mortgage Loan Underwriter

Adapting to the Future

Conclusion In conclusion, becoming a mortgage loan underwriter in an era dominated by automated systems like DU or LP presents a unique set of challenges and opportunities. The role is evolving, but far from diminishing in importance. With the right skills and mindset, a career in mortgage loan underwriting can be both rewarding and secure, offering a blend of technological engagement, intellectual challenge, and real-world impact.

In the mortgage industry rates will usually determine our loan activity and ultimately our income as mortgage loan originators. We generally rely on our company pricing bulletins or loan pricing engines to obtain the day's current rates. Many MLOs do independent research to better understand what drives these interest rates and try to predict whether the rates may rise or fall in short and long term. But what really goes into determining the day's mortgage rates? What factors can we look at to determine, for ourselves, what is likely to happen with interest rates int he future? These questions are not easily answered, but here is an overview of what affects mortgage interest rates and what experts look to when speculating on future interest rates. Anatomy of Mortgage Interest Rates Lender's Deliberations Mortgage interest rates are meticulously calibrated by lending institutions, each using a unique blend of considerations when setting rates. Understanding the lender's perspective is important:

Navigating Market Forces Lenders do not operate in a vacuum; they are uniquely linked to a dynamic market ecosystem. These external forces exert significant influence on mortgage rates:

Nuances in Rate Determination Borrower-Centric Factors While lenders set the stage, individual borrowers are a participant in the mortgage rate process. Their creditworthiness and financial profiles contribute to rate variance:

The Impact of Loan Size The size of the loan, often measured by the loan-to-value (LTV) ratio, can also affect mortgage rates. Loans with higher LTV ratios may be subject to higher rates as they are perceived as riskier loans. Advanced Tools and Strategies for Rate Prediction The Economist's Toolkit Economists and industry experts employ a sophisticated toolkit of economic indicators to forecast mortgage rates with precision:

The Importance of Yield Curve Monitoring the yield curve is a potent predictive tool. An inverted yield curve, where short-term rates surpass long-term rates, can predate economic downturns and lower future mortgage rates. The Central Bank Voice Industry experts closely scrutinize central bank communications and policy decisions. Statements and actions from central banks, notably the Federal Reserve, provide invaluable insights into future rate trajectories. The Science of Models and Data Analysis Intricate financial models, including econometric models and interest rate models, scrutinize historical data and complex economic relationships to offer predictive accuracy. These models integrate and array of economic variables, allowing experts to anticipate future mortgage rates with precision. For example, the term structure of interest rates can be modeled using techniques like the Nelson-Siegel model or the Vasicek model. These models attempt to capture the relationship between short-term and long-term interest rates. The Role of External Factors Geopolitical Unrest Geopolitical tensions and global events can significantly impact mortgage rates. Conflicts, trade disputes, and political instability can lead to market volatility, influencing rate movements. Market Sentiment Investor sentiment and market psychology can also affect rates. News, market speculation, and shifts in investor confidence can lead to sudden rate fluctuations. Technological Advancements Emerging technologies, such as blockchain and digital lending platforms, are reshaping the mortgage industry. These innovations can influence the efficiency of lending processes and, in turn, affect rate dynamics. The Regulatory Landscape Changes in financial regulations and government policies can have a profound impact on mortgage rates. Industry experts closely monitor legislative developments and regulatory changes for their potential influence on interest rates. Forecasting and Managing Rate Risk The ability to forecast and manage interest rate risk is paramount for industry experts. Sophisticated risk management strategies, including interest rate hedging and derivatives, are essential tools for mitigating the impact of rate fluctuations on portfolios and financial institutions. Conclusion For industry experts in the mortgage and real estate finance sectors, understanding the mechanics and influences behind mortgage interest rates is indispensable. The understanding of how complex factors drive rate determination, the tools and strategies employed for rate prediction, and the critical role external factors play in determining our daily mortgage rates. What is devoid in the process is a mortgage loan originator's influence int he interest rate process. Only with knowledge and an understanding of the complexities of mortgage interest rates, can professionals make informed decisions and seize opportunities when they occur.

|